Auto Industry Facing High Demand, Thanks to U.S. Resurgence

Long before the U.S. economy slipped into recession in 2008, the once-dominant “Detroit Three (D3)”—Ford, Chrysler, and GM—were losing market share at a rapid pace. In the 1980s, competition from international and other automakers just entering the U.S. market drastically changed the business of selling cars here, but the D3 never quite adapted to this new business environment.

The “Great Recession” proved too much for the D3, sending Chrysler and GM into bankruptcy, with Ford not far behind.

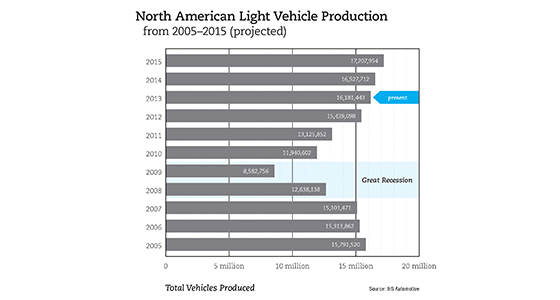

How bad did it get? According to the global market information and analytics leader IHS, over 17 million light vehicles were produced in North America in 2000. Of this, 76 percent were produced by the D3, with the remaining 24 percent produced by international and other domestic automakers.

By the end of the recession in 2009, total light vehicle production dropped by over 8.5 million units, with the D3 making just 55 percent of these vehicles. While the majority of U.S.-based manufacturers experienced significant production declines, international automakers were now accounting for a much larger piece of the pie.

Fast forward to 2013: U.S. automotive sales are on the rebound, and the D3 are healthier than they have been in a very long time. The industry as a whole is on pace to produce over 16 million light vehicles by the end of this year, and the D3 are maintaining their share of this production at 55 percent.

International automakers with U.S. manufacturing operations—BMW, Hyundai, Nissan, Toyota, Volkswagen, among others—took measures to lessen the impact of the recession, like cutting overtime and holding periodic plant shutdowns, leaving them virtually unscathed at the recession’s end.

While the D3 are no doubt healthier, IHS projections show a steady decline in their percentage of light vehicle production share through 2020.

Michael Robinet, managing director of automotive for IHS, has a deep understanding of the ebbs and flows of the automotive market, having developed global vehicle production forecasts for IHS for 15 of his 25 years with the group. This forecast is used by 85-to-90 percent of the world’s vehicle suppliers to make decisions about production planning and capital investments. According to Robinet, international automakers are increasingly shifting production of once-imported vehicles to the U.S., which would account for the D3’s overall percentage decrease in production rates here. And, because foreign-based manufacturers are largely hubbed in markets outside the U.S., they were not as adversely impacted by the U.S. economic downturn.

While the government bailout helped the D3 pay off a large percentage of their debt and invest in technology and equipment, he attributes their newfound success to a complete mindset change.

“You had vehicle manufacturers that were burdened with higher labor costs,” explained Robinet. “They had high fixed and high capital costs. They were spending too much to develop their vehicles because they couldn’t spread those development costs on a global perspective—they could only spread them from a regional perspective. So the economics were backwards, but also the structure needed to be updated to the 21st century.”

Robinet contends that “to move the metal,” the D3 began driving vehicle prices down with incentives rather than finding ways to cut production costs. So when the economy tanked and there was less consumer purchasing power, incentives did not move cars off lots the way they once did, forcing these automakers to make critical changes to the way they do business.

“Basically, they had to start from the bottom and really work their way through and ask, ‘what do we really need to do to make this company better, faster, less costly, and more flexible,’ ” said Robinet.

Today, Robinet says the D3 are much more disciplined about their pricing structures, only adding incentives when absolutely necessary. And now that the emphasis is off incentive programs, it has freed them to focus on product innovation and improving plant efficiencies, bringing them closer to par with their international counterparts.

Historically, Robinet says an average workweek for a U.S. automotive plant was around 80 hours, but today’s U.S. automakers—both domestic and international alike—have some plants producing vehicles up to 130 hours each week.

“If you think about capacity on a two-shift basis that means that you’re basically using your plant at 150 percent capacity… that’s not something just nice to have… that’s a mindset change. And then, if the demand goes down, you just ratchet it back.”

While a U.S. automotive resurgence is undeniable, new challenges lie ahead for both domestic and international manufacturers, mostly notably new, stricter regulations from the Environmental Protection Agency (EPA) to curb vehicle emissions.

“The fact is that we need to take 25-to-30 percent of the mass out of our vehicles by 2025 or so, and a lot of heavy lifting has to occur between now and then,” explained Robinet. “It’s more than changing from steel fenders to aluminum fenders. It goes a lot deeper than that. It’s changing the manufacturing philosophy, it’s changing the supply base, it’s changing the way you develop vehicles.”

- Category:

- GrayWay

- Industry

- Manufacturing

Some opinions expressed in this article may be those of a contributing author and not necessarily Gray.

Related News & Insights

Advanced Technology, Construction

Why Industrial Projects Should Align Design & Construction Early

Industry

July 08, 2026Advanced Technology, Construction

5 Common Problems That Slow Construction—and How Your Business Can Avoid Them

Industry

July 06, 2026Data Centers

Today's Cleanroom Construction Projects Pave the Way for Tomorrow's Technology

Industry

June 04, 2026